Returns are due at the end of the month for the previous month. See the example below.

Reporting Period

Period End Date

Due Date

Every Month (for example, June)

Last day of current month (June 30)

Last day of the following month (July 31)

Yearly Reporting Basis (For Sales Tax Accounts)

Reporting Period

Period End Date

Due Date

January – December

December 31

January 31

Yearly Reporting Basis (For Qualified Purchasers and Consumer Use Tax Accounts)

Reporting Period

Period End Date

Due Date

January – December

December 31

April 15

If you are required to file on a yearly reporting basis and you sell or discontinue operating your business, then you are required to file a final tax return. It is important that you file the return and pay any taxes due on time to avoid penalty and interest charges.

A final return for an account reporting on a yearly basis covers the period from January 1 through the date the business is discontinued. The final return must be filed and the taxes paid according to the schedule shown below.

If the business discontinues between:

The due date of the final return is:

January – March

April 30

April – June

July 31

July – September

October 31

October – December

January 31

Fiscal Yearly Reporting Basis

Reporting Period

Period End Date

Due Date

July – June

June 30

July 31

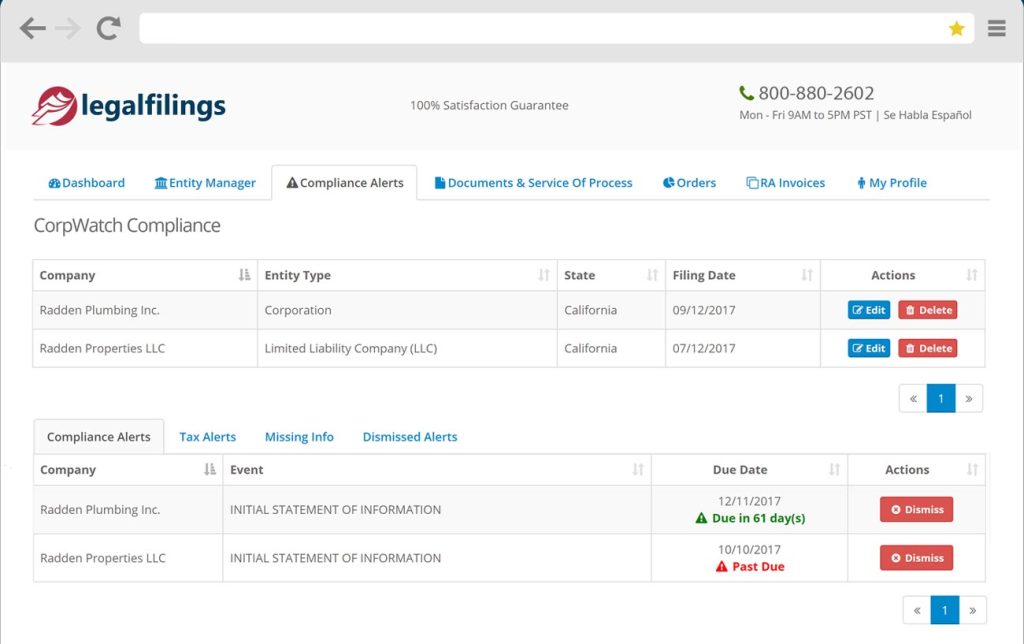

CorpWatch™ Compliance

Included is our advanced compliance monitoring portal which will track deadlines for filing state taxes and maintenance filings for your business.

Generally, if you make three or more sales in a 12-month period in California, you are required to hold a seller’s permit. This applies even if your sales are made through Internet auction houses or websites that offer online classified advertisements (online advertisers).

When you have a garage sale and sell used items, you are generally not required to hold a seller’s permit unless you have more than two garage sales in a 12-month period or are required to hold a seller’s permit for being engaged in the business of selling merchandise, goods, or items (tangible personal property).

Making sales of merchandise, goods, or other items in California without first getting a seller’s permit violates the law and subjects you to fines and penalties. California law requires a seller’s permit to be held for warehouse locations when: the retailer has one or more sales offices in this state, the sale is negotiated out of state, and the order is filled from the retailer’s in-state stock of goods at the warehouse. You are not required to hold a seller’s permit if all your sales are made exclusively in interstate or foreign commerce, and you make no sales in this state. However, your business may be required to register for a use tax account.

When you hold a seller’s permit, you must file sales and use tax returns and pay any sales or use tax due on your sales and purchases. You must report and pay sales tax on each taxable sale. When you make the sale, you may collect from your customer an amount equal to the tax you will owe. You also must keep adequate records that document your sales and purchases. As a registered seller, you will need to take the time to learn how to properly apply the sales and use tax law in your business operations. View the seller’s permit compliance requirements here.

You should not obtain a seller’s permit just to take advantage of the opportunity to issue resale certificates to your suppliers. Issuing a resale certificate to avoid paying tax on items you will use rather than sell is against the law and may result in fines and penalties.

Why Legalfilings

We’re entrepreneurs — just like you. We understand that your business is constantly evolving, and so are we. Our team is dedicated to staying ahead of the curve and keeping you informed on all the latest news, insights, and resources for entrepreneurs.

We’re passionate about entrepreneurship, and we’re here to help you achieve your dreams. Thanks for being part of the community!